Three insurance appetite guide – The insurance industry operates on a complex system of risk assessment and acceptance. A crucial component of this system is the insurer’s “appetite,” which defines the types and levels of risk they are willing to underwrite. Understanding an insurer’s appetite is critical for brokers, agents, and businesses seeking insurance coverage. This guide delves into the three key aspects of an insurance appetite: risk appetite, capacity, and tolerance.

1. Risk Appetite

Defining the Boundaries

Risk appetite forms the core of an insurer’s underwriting philosophy. It represents the organization’s overall willingness to accept risk in pursuit of profit. This is not a static concept; it evolves based on various internal and external factors, including market conditions, regulatory changes, and the insurer’s financial stability. A high-risk appetite indicates a willingness to underwrite policies with potentially higher payouts, while a low-risk appetite favors policies with lower risk profiles.

Factors Influencing Risk Appetite:

- Financial Strength: Insurers with strong capital reserves can generally afford to accept higher levels of risk.

- Market Conditions: Competitive pressures and economic downturns can influence an insurer’s willingness to take on risk.

- Regulatory Environment: Changes in insurance regulations can impact an insurer’s risk appetite, potentially leading to stricter underwriting guidelines.

- Investment Strategy: The insurer’s investment portfolio can influence its risk tolerance and overall appetite for underwriting new business.

- Reinsurance Capacity: Access to reinsurance significantly impacts an insurer’s ability to manage and absorb large losses, thus influencing their risk appetite.

2. Capacity

The Limits of Underwriting

Capacity refers to the insurer’s ability to underwrite new business. It’s a measure of their financial resources, including capital, surplus, and reinsurance capacity. Capacity sets a practical limit on the volume and size of risks an insurer can accept. Even if an insurer has a high risk appetite, its capacity might constrain the amount of risk it can underwrite.

For example, a small insurer might have a high appetite for commercial real estate insurance but lack the capacity to underwrite large, multi-million dollar policies.

Factors Determining Capacity:

- Capital Reserves: The amount of capital an insurer holds directly influences its capacity to absorb potential losses.

- Reinsurance Agreements: Reinsurance significantly expands an insurer’s capacity by transferring a portion of the risk to another insurer.

- Investment Returns: Investment income contributes to an insurer’s overall financial strength and thus its underwriting capacity.

- Loss Ratios: High loss ratios can reduce an insurer’s capacity by consuming capital reserves.

- Regulatory Requirements: Solvency regulations set minimum capital requirements, influencing the insurer’s capacity.

3. Risk Tolerance

Source: slidesharecdn.com

The Acceptable Level of Loss

Risk tolerance represents the maximum level of loss an insurer is willing to accept. It’s closely related to risk appetite but focuses specifically on the potential financial impact of adverse events. A high risk tolerance suggests the insurer is prepared to absorb larger losses, while a low risk tolerance implies a greater emphasis on loss prevention and mitigation.

Risk tolerance is often expressed as a percentage of capital or surplus.

Understanding the Interplay:

Risk appetite, capacity, and tolerance are interconnected. An insurer’s appetite sets the strategic direction, capacity defines the practical limits, and tolerance sets the acceptable level of financial impact. These three elements work in concert to shape an insurer’s underwriting decisions. A mismatch between these factors can lead to financial instability. For instance, an insurer with a high appetite but low capacity might overextend itself, leading to financial difficulties.

Source: financialcrimeacademy.org

Analyzing an Insurer’s Appetite: Practical Applications

Understanding an insurer’s appetite is crucial for various stakeholders. Brokers and agents can use this knowledge to match clients’ needs with appropriate insurers. Businesses seeking insurance can leverage this information to improve their chances of securing coverage. Analyzing an insurer’s appetite involves reviewing their financial statements, understanding their underwriting guidelines, and examining their historical loss data.

Key Indicators of Insurance Appetite:, Three insurance appetite guide

- Underwriting Guidelines: These documents Artikel the specific types of risks an insurer is willing to accept.

- Financial Statements: Analyzing an insurer’s financial health provides insights into their capacity and risk tolerance.

- Loss Ratios: A high loss ratio might indicate a lower risk tolerance or capacity.

- Market Share: An insurer’s market share in specific segments can reflect its appetite for those types of risks.

- Public Statements: Insurers sometimes publicly discuss their strategic priorities, which can offer clues about their risk appetite.

Frequently Asked Questions (FAQ)

- Q: How does reinsurance affect an insurer’s appetite?

A: Reinsurance significantly expands an insurer’s capacity, allowing them to take on more risk than they could otherwise afford. This can lead to a higher risk appetite, as they can transfer a portion of the potential losses to a reinsurer. - Q: What happens if an insurer’s appetite changes?

A: A change in appetite can lead to adjustments in underwriting guidelines, potentially resulting in changes to pricing, coverage availability, and acceptance criteria for certain risks. - Q: How can I find information about an insurer’s appetite?

A: Information on an insurer’s appetite can be found through their annual reports, underwriting guidelines (if publicly available), industry publications, and discussions with insurance brokers or agents. - Q: What is the difference between risk appetite and risk tolerance?

A: Risk appetite is the overall willingness to accept risk, while risk tolerance is the maximum level of loss an insurer is willing to absorb. Appetite sets the strategic direction, while tolerance focuses on the financial impact of losses. - Q: How does economic downturn impact an insurer’s appetite?

A: During economic downturns, insurers often become more risk-averse, reducing their appetite and tightening their underwriting standards due to increased uncertainty and potential for higher claims.

References

Call to Action: Three Insurance Appetite Guide

Understanding the intricacies of insurance appetite is crucial for navigating the insurance landscape effectively. By grasping the interplay between risk appetite, capacity, and tolerance, you can make more informed decisions, whether you’re a broker, agent, or business seeking insurance coverage. Contact us today to learn more about how we can help you understand and leverage this critical aspect of the insurance industry.

Frequently Asked Questions

What is an insurance appetite statement?

An insurance appetite statement formally documents an organization’s risk tolerance levels, outlining the types and sizes of risks it’s willing to underwrite or insure.

How often should an insurance appetite be reviewed?

An insurance appetite should be reviewed at least annually, or more frequently if significant changes occur in the market, regulatory landscape, or the organization’s financial position.

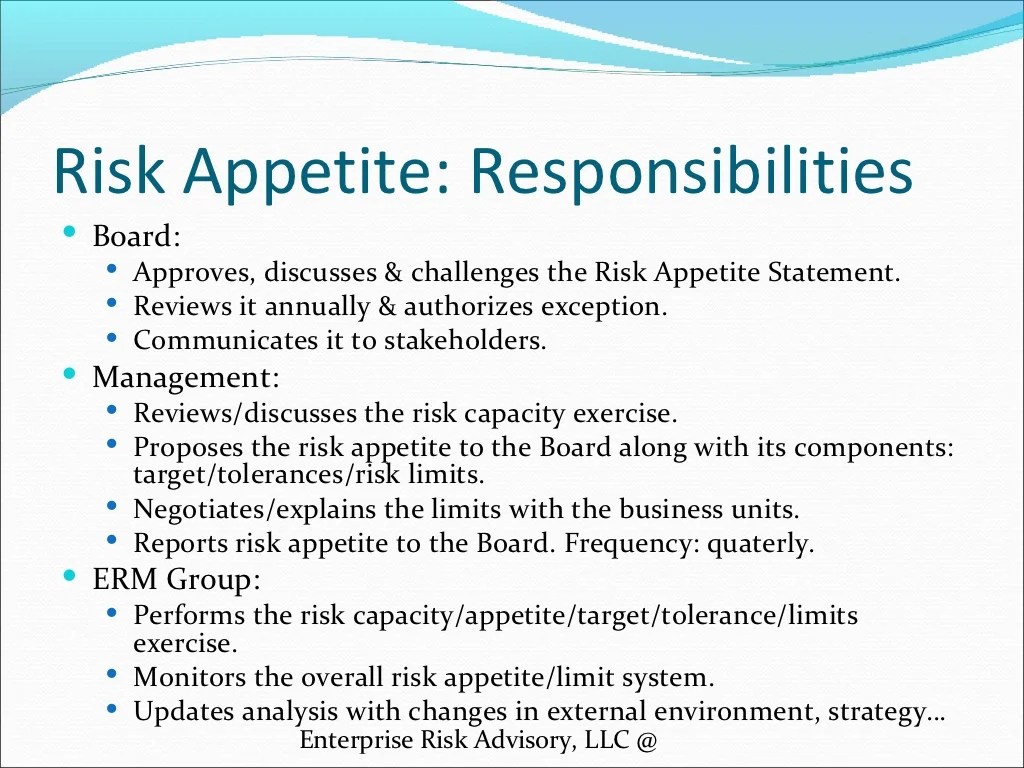

Who is responsible for managing insurance appetite?

Responsibility usually lies with senior management, risk management teams, and underwriting departments, working collaboratively.