Is cit fdic insured – The safety and security of your hard-earned money are paramount. Many people assume that because their funds are in a financial institution, they are automatically protected. While this is often true for deposits in banks, the situation with credit unions requires a closer look. This comprehensive guide will delve into the details of FDIC insurance, explain whether credit unions are covered, and clarify what protection you have for your deposits.

The Role of the FDIC: Protecting Bank Deposits

The Federal Deposit Insurance Corporation (FDIC) is an independent agency of the U.S. government created in 1933 in response to the Great Depression. Its primary purpose is to maintain stability and public confidence in the nation’s financial system by insuring deposits in banks and savings associations. This insurance protects depositors from losses if their bank fails.

What Does FDIC Insurance Cover?

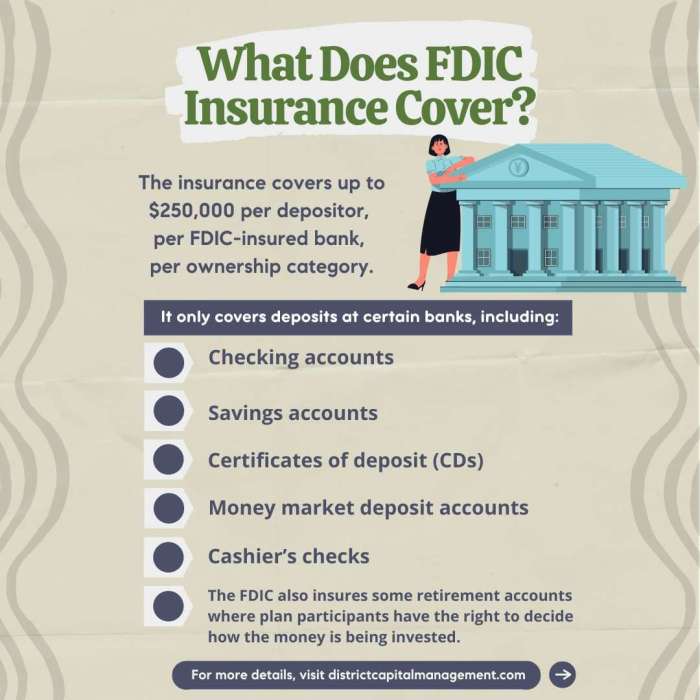

FDIC insurance typically covers deposit accounts, including checking accounts, savings accounts, money market accounts, and certificates of deposit (CDs). However, there are limits to this coverage. The standard coverage limit is $250,000 per depositor, per insured bank, for each account ownership category. This means that if you have multiple accounts at the same bank, the FDIC will insure each account up to $250,000, but it might be necessary to strategize your accounts to maximize coverage.

The FDIC website offers resources to help understand how this works.

Understanding Account Ownership Categories

The FDIC’s insurance coverage is categorized based on ownership. Different ownership categories include single accounts, joint accounts, revocable trust accounts, and employee benefit plan accounts. Each category is insured separately up to the $250,000 limit. Understanding these categories is crucial for maximizing your FDIC insurance coverage. For instance, a joint account with two owners may have a higher coverage limit than a single account.

Credit Union Insurance: The National Credit Union Administration (NCUA)

Unlike banks, credit unions are not insured by the FDIC. Instead, they are insured by the National Credit Union Administration (NCUA). The NCUA is an independent federal agency that regulates and charters federal credit unions and insures the deposits in all federal and most state-chartered credit unions.

NCUA Insurance: Similar to FDIC Coverage

The NCUA’s insurance coverage, known as Share Insurance, is very similar to FDIC insurance. It provides the same level of protection for deposits in credit unions, offering a standard coverage limit of $250,000 per depositor, per insured credit union, for each account ownership category. Just like with FDIC insurance, understanding account ownership categories is vital for maximizing your coverage.

How to Verify Your Credit Union’s Insurance

It’s always a good idea to verify that your credit union is NCUA insured. You can check this easily on the NCUA’s website using their “Where’s My Money?” tool. This tool allows you to search for your credit union by name or location and confirm its insurance status. Don’t hesitate to contact your credit union directly if you have any questions about their insurance coverage.

Source: johnsonfinancial.com

Maximizing Your Deposit Insurance Coverage

Given the $250,000 limit per depositor, per insured institution, per account ownership category, it’s essential to understand strategies for maximizing your coverage. This may involve diversifying your deposits across multiple institutions or utilizing different account ownership categories.

Strategies for Higher Coverage, Is cit fdic insured

- Multiple Institutions: Spreading your deposits across several FDIC-insured banks or NCUA-insured credit unions increases your overall coverage.

- Multiple Account Ownership Categories: Utilizing different account ownership categories (single, joint, etc.) can significantly increase your insured amount.

- Consult a Financial Advisor: For complex financial situations, consulting a financial advisor can help you develop a comprehensive strategy for maximizing your deposit insurance coverage.

Understanding the Limits of Deposit Insurance

It’s crucial to remember that deposit insurance only covers deposits. It does not cover investments such as stocks, bonds, or mutual funds held through the financial institution. Additionally, it doesn’t protect against losses due to market fluctuations or fraud outside the institution’s control.

Frequently Asked Questions (FAQs)

- Q: Is my money safe in a credit union? A: Yes, your money in an NCUA-insured credit union is safe up to the $250,000 coverage limit.

- Q: What is the difference between FDIC and NCUA insurance? A: The FDIC insures deposits in banks, while the NCUA insures deposits in credit unions. Both offer similar levels of protection.

- Q: How can I check if my credit union is insured? A: You can verify your credit union’s insurance status on the NCUA website.

- Q: What if I have more than $250,000 in a credit union? A: You should consider spreading your deposits across multiple NCUA-insured credit unions or utilize different account ownership categories to maximize coverage.

- Q: Does deposit insurance cover all types of accounts? A: Generally, yes, but it’s essential to check the specific terms and conditions of your institution’s insurance coverage.

Conclusion

Understanding deposit insurance, whether through the FDIC or the NCUA, is vital for protecting your savings. While both offer robust protection, it’s crucial to be aware of the coverage limits and strategies for maximizing your protection. Always verify your institution’s insurance status and don’t hesitate to contact them or the relevant regulatory agency if you have any questions.

References: Is Cit Fdic Insured

Call to Action

Protect your financial future! Verify your institution’s insurance coverage today and explore strategies to maximize your deposit insurance protection. Contact your financial institution or a financial advisor for personalized guidance.

Answers to Common Questions

What types of accounts at CIT Bank are FDIC insured?

Source: estradinglife.com

Generally, checking accounts, savings accounts, and money market accounts are FDIC insured up to the maximum limit.

Is there a limit to FDIC insurance coverage?

Yes, the FDIC currently insures deposits up to $250,000 per depositor, per insured bank, for each account ownership category.

What happens if CIT Bank fails?

If CIT Bank were to fail, the FDIC would step in to ensure depositors receive their insured funds. The process typically involves transferring accounts to another institution.

How can I verify my FDIC insurance coverage?

Source: districtcapitalmanagement.com

You can verify your coverage by checking your account statements or contacting CIT Bank’s customer service directly.